Market + AI Trend Intelligence

AI Answer Accuracy in ASEAN Financial Services — Singapore and Malaysia So Far

How accurately public AI answers questions about banks and insurance schemes across Singapore and Malaysia. A cross-market Lawnise barometer.

Lawnise Research & Editorial team

Institutional byline · published by Lawnise

Someone in Singapore is weighing a cash advance. Someone in Kuala Lumpur is waiting on a card application and wants to know how long the bank has to decide. Someone else is reading up on a public disability scheme before a parent needs it. None of them open the bank's tariff sheet or the scheme's official page first — they ask a public AI assistant, and they get back an answer that sounds settled: a clean figure, a confident timeline, a tidy summary of who's covered. The fact being described is a public one, and it is on the record correctly. We have been checking, scope by scope, whether the answer matches that record.

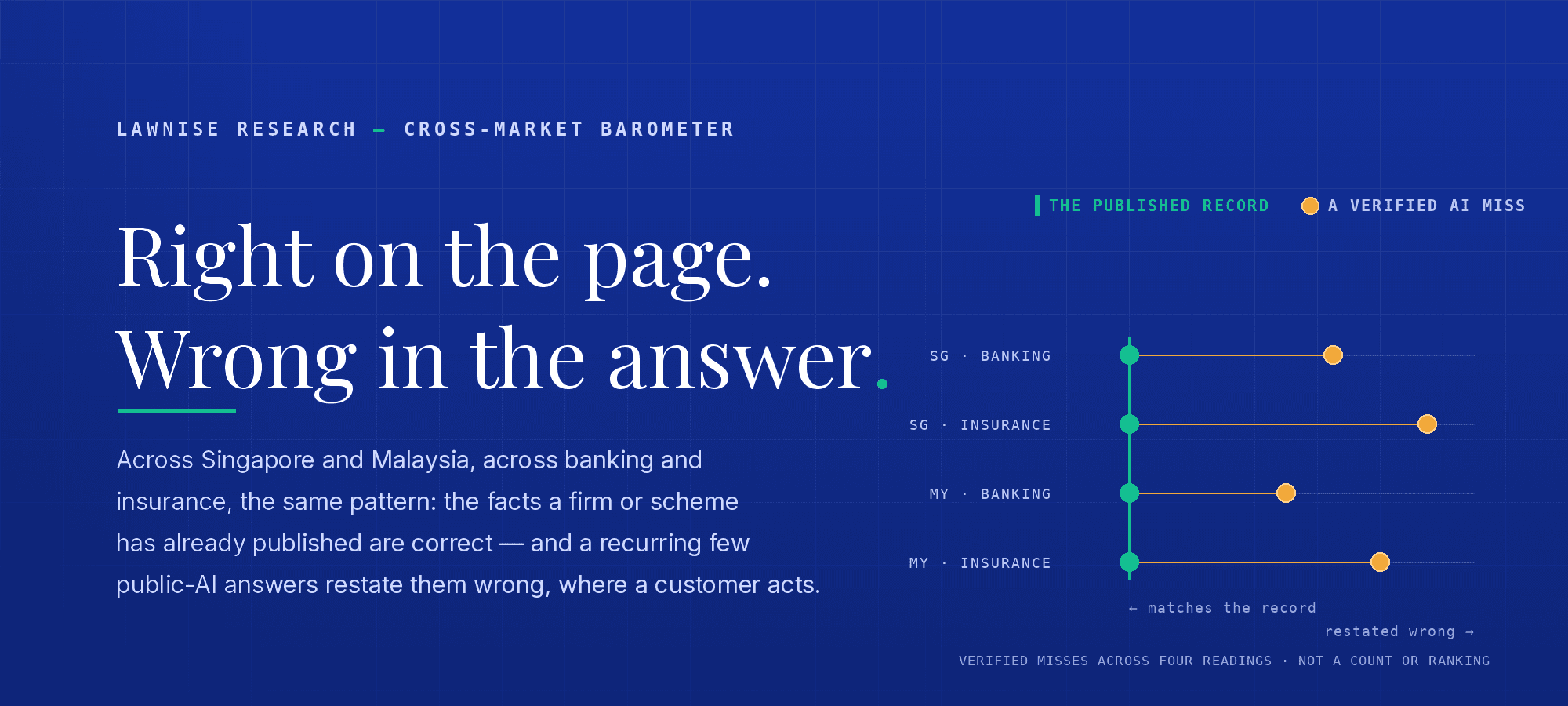

This is the overview that sits above our individual barometer readings. Each reading takes one market and one sector and checks public AI answers against the published record there. Read together, the readings so far — Singapore banking, Singapore insurance, Malaysian banking, Malaysian insurance — point at the same thing, and that common pattern is what this page is for. With those four readings the two-market, two-sector grid is now complete — both sectors read across both markets — and the overview stays living: we expect the shape to hold or shift as we add new periods and categories.

How we read AI answer accuracy across Singapore and Malaysia

Each reading follows the same shape. We put high-intent questions — the kind a customer types before opening a product, disputing a charge, or working out whether a scheme will help — to a set of public AI systems, among them ChatGPT, Gemini, Copilot, Perplexity, Grok and Google AI Overview. We then compare each answer against the institution's or scheme's own published facts: the disclosure sheet, the product page, the policy, the official scheme page. Where an answer conflicts with the published record, we flag it, and we hand-verify each finding against the live source before it earns a place in a reading.

A few things are worth saying about what this overview is and isn't. It carries a pattern, not a number. We do not publish a cross-scope accuracy rate, or a count of answers, or anything that reads as "X% across the series" — that would imply a measurement we have not run. What we do instead is synthesise the pattern qualitatively and illustrate it with the specific, verified findings from each reading, each one attributed to the reading it came from. We name the AI systems only as the set we tested, never to rank one against another. The banks we leave unnamed by design; the public schemes we name, because they are public programmes any reader can look up. The underlying evidence and result identifiers are retained internally for audit and right-to-reply.

The pattern across markets and sectors

Read on their own, each reading looks like a local story: a Singapore card rate here, a Malaysian service timeline there, an insurance threshold somewhere else. Read together, they rhyme. Across the readings, public AI was not uniformly wrong: the spoke articles record correct or near-correct answers alongside the misses. But a recurring few missed, and they missed in a consistent way: a public fact, already correct on the institution's or scheme's own page, restated as something the customer would act on differently.

In Singapore banking, the misses clustered on the cost of borrowing. One major Singapore bank publishes a cash-advance rate of 28.5% per annum; every system that committed to a specific rate came back below it, 26.9% at the lowest. At a different Singapore bank, a published card rate of 27.9% a year was quoted by one assistant as 15–18% — roughly half. The published figures were right; the answers a customer would have planned around were cheaper than the real cost of borrowing.

In Singapore insurance, the same shape showed up against public schemes — and here the facts are not just published but named programmes. CareShield Life's severe-disability payout triggers at the inability to perform 3 of 6 activities of daily living; one system described the trigger as just 1. FIDReC adjudicates disputes up to S$150,000; one system put the limit at S$500,000. And the FIDReC-NIMA motor scheme, which covers only non-injury third-party claims below S$3,000, was described by one system as broadly available. A reader trusting those answers would misjudge what a scheme protects them against, and where a grievance can actually go.

In Malaysian banking, the misses gathered on service timelines. Banks' published customer-service charters commit to deciding a credit-card application within 3 working days; customers were told 5–7 days, 7–10 days, even 2–3 weeks, though one system did land near the published commitment. A 5-working-day mortgage commitment was described by one system as about 30 days, and a 14-calendar-day complaint-decision commitment as 20 working days. Each answer set an expectation slower than the charter the bank actually publishes.

In Malaysian insurance, the misses landed on a named public scheme — PIDM's Takaful and Insurance Benefits Protection System (TIPS), which protects eligible benefits up to RM500,000 if an insurer fails. Where policies share the same insurer member, the same risk event, the same life insured and the same policy owner, the benefits aggregate into one RM500,000 limit — so three same-insurer death-benefit policies on one life share a single ceiling, not three. One system described the limit as applying per policy, which would let a consumer with three believe RM1.5 million was protected. And the life and death-benefit limit, which is RM500,000, was stated by one system as RM250,000 — the figure from PIDM's separate bank deposit-insurance scheme — understating the protection by half. The scheme's own pages were right; the answers a consumer would lean on either over- or under-stated what TIPS would actually cover.

Put the four side by side and the through-line is hard to miss. Two markets, two sectors, different facts each time — a borrowing rate, a payout trigger, an adjudication limit, a service deadline, a protection limit — and in each case the published record was right and the version circulating in AI answers was not. The errors point in different directions: a rate quoted too low, a coverage trigger quoted too easy, a timeline quoted too slow, a protection limit quoted both too high and too low. What they share is that none of them sit in what the institution published. They sit in how a public system restated it.

Why this is a cross-sector governance risk

What makes this a governance question rather than a curiosity is that it crosses lines a single institution's controls were built around. A Singapore bank can keep its tariff sheet immaculate, a Singapore scheme can keep its eligibility page current, a Malaysian bank can hold to its service charter — and a customer can still arrive having been told a borrowing cost below the real one, a coverage trigger easier than the real one, or a service deadline slower than the real one, by a system the institution has no contract with and no visibility into. The record was right. The representation circulating about it was not. None of these answers were written by the institution, and none can be edited by it the way its own website copy can.

Most governance frameworks weren't built to see this. They scrutinise what the institution publishes — and the publishing, in every reading so far, was correct. The risk lives one step outside that perimeter, in the growing share of customers who ask a public AI before they ask the bank or read the scheme. Because the pattern repeats across markets and sectors, it isn't a quirk of one product or one regulator's disclosure rules; it travels with the channel. The consequences — confusion, an avoidable complaint, a fair-dealing question about information circulating in the institution's name — are the institution's to understand, evidence, and manage, regardless of who typed the answer.

How to govern AI answers about your institution

The answer isn't to chase the AI, which can't be corrected the way owned website copy can, but to govern the surface with the same seriousness applied to any channel that speaks in the institution's name. In practice that's a repeatable loop: watch what the major systems are telling customers about your products and obligations; check it against your own published facts; separate the genuine misstatements from the false alarms before acting on either; work out why a real one drifted, since a stale source and outside misinformation call for different fixes; rank what could actually mislead a customer — a borrowing cost quoted at half, a coverage trigger quoted too easy — ahead of what's merely imprecise; and keep a dated record of what was said and when. Done steadily, an open-ended worry becomes a managed process: the institution finds out before the customer does, corrects the sources it controls, and can show its work to a board, or to a regulator, when asked what it is doing about AI.

The cross-market pattern is also the practical case for not treating this market by market. A risk owner reading only the banking finding might file it as a pricing-disclosure issue; reading only the insurance finding, as a scheme-eligibility issue. Read together, they describe one exposure with several faces, and an institution that watches the surface in one sector or one country has a head start on the next.

Read the barometer readings

Each reading carries its own verified findings, its sources, and its own measured read of where the answers held and where they drifted: AI answer accuracy in Singapore banking, AI answer accuracy in the Singapore insurance sector, AI answer accuracy in Malaysian banking, and AI answer accuracy in Malaysian insurance. With banking and insurance now read across both markets, the overview will grow as new periods and categories publish.

If you'd like to see what public AI is currently saying about your own institution — checked, the way these were, against your own published facts — we can scope a private baseline: sector-context, no obligation.

How to cite this

- Short form

- Lawnise Research & Editorial team. (2026). AI Answer Accuracy in ASEAN Financial Services — Singapore and Malaysia So Far. Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-asean-financial-services

- Long form (APA)

- Lawnise Research & Editorial team. (2026, June 18). AI Answer Accuracy in ASEAN Financial Services — Singapore and Malaysia So Far (Methodology v1.1). Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-asean-financial-services

- BibTeX

@misc{lawnise2026aiansweraccuracyaseanfinancialservices, author = {Lawnise Research and Editorial team}, title = {AI Answer Accuracy in ASEAN Financial Services — Singapore and Malaysia So Far}, year = {2026}, publisher = {Lawnise}, url = {https://www.lawnise.com/research/ai-answer-accuracy-asean-financial-services} }

References

- [1]Lawnise Methodology (v1.1). This overview synthesises four published Lawnise barometer readings (Singapore banking, Singapore insurance, Malaysian banking, Malaysian insurance). Each featured finding was true-positive verified in its reading — quote-grounded in the AI's full response and confirmed against the institution's or scheme's live published source — before publication. We carry the verified specifics and the cross-market pattern, not a cross-scope accuracy rate. Banks are unnamed by research design; public schemes are named. Evidence and result identifiers are retained internally for audit and right-to-reply. https://www.lawnise.com/trust-index/methodology/v1#main

- [2]CPFB / MOH, Singapore. CareShield Life severe-disability payouts trigger at the inability to perform 3 of the 6 Activities of Daily Living. https://www.cpf.gov.sg/member/healthcare-financing/careshield-life(accessed 2026-06-24)

- [3]Financial Industry Disputes Resolution Centre (FIDReC). FIDReC's adjudication limit is S$150,000 per claim (since 1 July 2024). https://www.fidrec.com.sg/knowledgebase/article/KA-01013/en-us(accessed 2026-06-24)

- [4]Financial Industry Disputes Resolution Centre (FIDReC). The FIDReC-NIMA scheme covers non-injury motor accident disputes below S$3,000, for claims against another party's insurer. https://www.fidrec.com.sg/knowledgebase/article/KA-01152/en-us(accessed 2026-06-24)

- [5]Perbadanan Insurans Deposit Malaysia (PIDM). Malaysia's TIPS (run by PIDM) protects eligible life-insurance death benefits up to RM500,000; protected benefits aggregate where they share the same insurer member, same risk event, same life insured, and same policy owner (RM250,000 is the separate bank deposit-insurance limit). https://www.pidm.gov.my/general/faqs/takaful-insurance-benefits-protection-system(accessed 2026-06-24)