Market + AI Trend Intelligence

The State of AI Answer Accuracy in Malaysian Banking — A Preliminary Barometer

A preliminary Lawnise study of how accurately public AI answers questions about Malaysian banks — where it restates published service commitments as longer or vaguer.

Lawnise Research & Editorial team

Institutional byline · published by Lawnise

A customer in Kuala Lumpur is about to apply for a credit card, and before filling in the form she asks a public AI assistant how long the bank will take to process it. The answer comes back clean and confident — a tidy number of working days. What she doesn't see is that the bank itself has already published a faster commitment, in plain terms, in its own customer service charter. The AI didn't invent a wait time out of nowhere. It restated a promise the bank had already made, only longer and vaguer than the bank made it. We checked answers like hers against those published commitments, one by one.

Public AI doesn't get Malaysian banking wrong across the board — these weren't uniform failures, and on some of the same questions other tested systems answered close to the published commitment. But a recurring few don't, and when they slip they tend to slip in one direction: the AI hands the customer a slower, softer version of a promise the bank already published. This matters most around the things a customer plans on — how long an application takes, how long a complaint has to be decided. This is one of several market-and-sector readings in our barometer, and it sits alongside our Singapore banking reading as a companion view of the same problem.

How we checked AI answers about Malaysian banks

In June 2026 we put high-intent retail questions — the kind a customer types before applying for a card or a loan, or before lodging a complaint — to a set of public AI systems, among them ChatGPT, Gemini, Copilot, Perplexity, Grok and Google AI Overview. Each answer about a Malaysian bank was compared against that bank's own published service commitment, set under the bank's published customer service charter — the industry framework Malaysian banks have published service timelines against since 2011. Where an answer stretched or softened the published commitment, we flagged it, and we hand-verified each finding against the bank's published service charter before standing behind it.

This is a preliminary reading, and we'd rather say so plainly than dress it up. It covers a single month, so it's a baseline rather than a trend. And we report patterns, not a scoreboard — we name the AI systems only as the set we tested, never to rank one against another, because the more useful question is what they get wrong in common. The individual banks we don't name, by research design: institution names are withheld to keep the reading anonymised, while the published standard itself is an industry-wide, public framework we can describe openly. We retain the underlying evidence and result identifiers internally, for audit and right-to-reply.

Where AI answers about Malaysian banks drift

A few things recurred often enough in Malaysian banking to be worth a risk owner's attention. These weren't cases where the bank's published commitment was wrong — it was right in every case. The quieter failure was a promise the bank put in writing, restated by the AI as longer or vaguer than the bank made it, in a place where a customer reads it, plans around it, and never learns the better version the bank actually published.

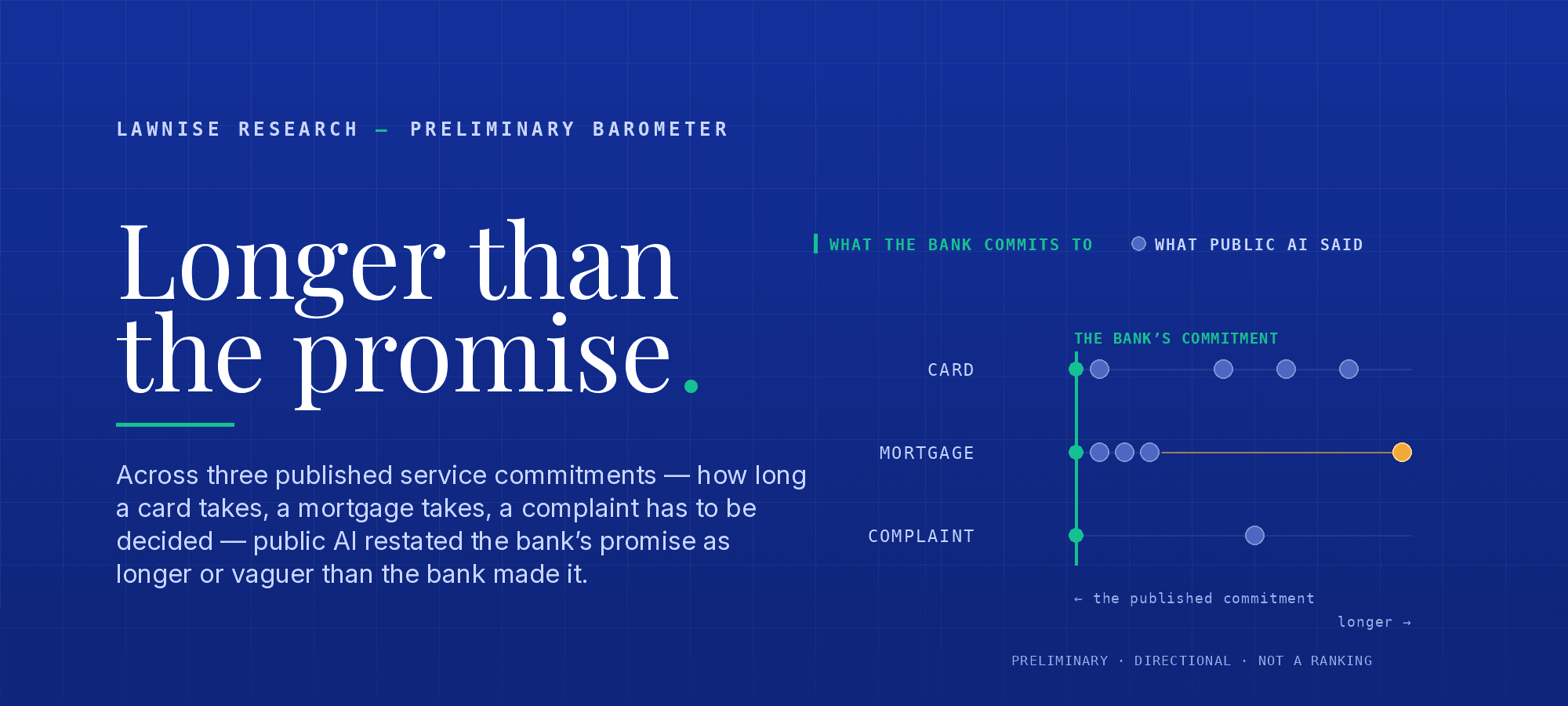

On a credit-card application, several systems told customers a slower timeline than the bank actually commits to. Under the industry's published service charter, a Malaysian bank commits to processing a credit-card application within 3 working days (plus mailing). Asked how long the bank takes, several systems overstated it — one answered 5–7 working days, another 7–10 working days, and one stretched it as far as 10–14 working days, or 2–3 weeks. In fairness, it wasn't every system: one answered the published commitment correctly, at about 3 working days. But a customer who is told two to three weeks may plan around that longer timeline — and never learn that the bank had committed, in writing, to a fraction of that.

On a mortgage, several systems answered near the mark — but one quoted six times the published commitment, twice. The same charter commits a bank to processing an individual home-loan application within 5 working days. Several of the systems we tested answered close to it, around five working days. But one told customers a mortgage takes about 30 days — roughly six times the published commitment — and gave that same answer for two different banks. A timeline overstated by that much isn't a footnote: it's the kind of figure that could send a customer to a different lender, or push a financing decision the wrong way, on the strength of a wait the bank never said it would take.

On a complaint, the AI gave the bank far longer to decide than the bank's own commitment allows. Under the published charter, a bank commits to inform a customer of its decision on a complaint no later than 14 calendar days from receipt. Asked the same question, one system said the bank takes 20 working days — roughly four weeks, and a different-market figure applied to a Malaysian question by mistake. The customer comes away thinking the bank has far longer to decide than it does — and never learns the 14-day commitment, or the right to escalate when it lapses. That's the failure that lands hardest: it surfaces exactly when a customer is already unhappy.

It isn't only timelines. Pricing facts drift in the same direction. Asked about an investment-financing product, one system quoted a profit rate as low as 3.45% per annum, when the bank's published rate is higher, around 4.45% per annum — understating the cost of borrowing rather than overstating it. The shape is the same as the timelines: a published figure restated as friendlier to the customer than the bank actually committed to, in a place where the customer reads it and plans around it.

Why AI answer accuracy is a governance risk for banks

None of these answers were written by the bank, and none of them can be edited by the bank the way its own website copy can. That's precisely the difficulty. A Malaysian institution can hold itself to the charter exactly — process the card in three working days, the mortgage in five, decide the complaint inside fourteen — and a customer can still arrive having been told the application takes two to three weeks, the mortgage thirty days, the complaint twenty, by a system the bank has no contract with and no visibility into. The published commitment was right. The version circulating about it was a degraded restatement. And the consequences — a customer who plans around the wrong timeline, an avoidable complaint, a fair-dealing question about information circulating in the bank's name — are the bank's to understand, evidence, and manage, regardless of who typed the answer.

Most governance frameworks weren't built to see this. They scrutinise what the institution publishes — and here the published record is accurate. The risk lives one step outside that perimeter, in the growing share of customers who ask an AI before they ask the bank, and learn a worse version of a promise the bank kept.

The Malaysian context makes the issue sharper. These commitments are published in the banks' own customer service charters, so a customer has a concrete promise to be measured against — and a concrete grievance when the AI restates it as something slower. The errors we saw aren't random noise: they cluster on processing times and on the handling of complaints, two areas where a misled customer plans around the wrong number and the bank carries a published obligation. A 3-working-day card commitment told as 2–3 weeks is the kind of thing a customer weighs before applying. A 5-working-day mortgage commitment told as 30 days is the kind of thing that changes which lender they choose. A 14-calendar-day complaint commitment told as 20 working days sets an expectation that buries the customer's own right to escalate. None of these is exotic; all are the everyday texture of retail banking, which is exactly why a degraded restatement of an ordinary commitment, circulating invisibly, is worth a risk function's time.

How to govern AI answers about your bank

The answer isn't to chase the AI, which can't be corrected the way the bank's own website copy can, but to govern the surface with the same seriousness applied to any channel that speaks in the bank's name. In practice that's a repeatable loop: watch what the major systems are telling customers about your timelines and your terms; check each answer against the bank's own published commitment; separate the genuine restatements-gone-wrong from the false alarms before acting on either; work out why a real one drifted, since a stale source and a cross-border mix-up call for different fixes; rank what could actually mislead a customer — a mortgage timeline told as six times the commitment, say — ahead of what's merely imprecise; and keep a dated record of what was said and when. Done steadily, an open-ended worry becomes a managed process — the institution finds out before the customer does, corrects the sources it controls, and can show its work to a board, or to a regulator, when asked what it's doing about AI.

Read on

This is an early read from an ongoing barometer Lawnise is building on how public AI answers questions about Malaysian banking, with more categories to follow over time. If you'd like to see what public AI is currently saying about your own institution — checked, the way these were, against your own published commitments — we can scope a private baseline: sector-context, no obligation.

How to cite this

- Short form

- Lawnise Research & Editorial team. (2026). The State of AI Answer Accuracy in Malaysian Banking — A Preliminary Barometer. Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-malaysia-banks

- Long form (APA)

- Lawnise Research & Editorial team. (2026, June 23). The State of AI Answer Accuracy in Malaysian Banking — A Preliminary Barometer (Methodology v1.1). Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-malaysia-banks

- BibTeX

@misc{lawnise2026aiansweraccuracymalaysiabanks, author = {Lawnise Research and Editorial team}, title = {The State of AI Answer Accuracy in Malaysian Banking — A Preliminary Barometer}, year = {2026}, publisher = {Lawnise}, url = {https://www.lawnise.com/research/ai-answer-accuracy-malaysia-banks} }

References

- [1]Lawnise Methodology (v1.1). Findings are drawn from a single-month capture in which high-intent retail-banking questions were put to a set of public AI systems, and each answer about a Malaysian bank was checked against that bank's own published customer service charter. Each featured finding was true-positive verified — quote-grounded in the AI's full response and confirmed against the published commitment — before publication. Banks are unnamed by research design; reported as directional patterns, not a ranking of AI systems. Underlying evidence and result identifiers are retained internally for audit and right-to-reply. https://www.lawnise.com/trust-index/methodology/v1#main