Market + AI Trend Intelligence

The State of AI Answer Accuracy in Singapore Banking — A Preliminary Barometer

A preliminary Lawnise study of how accurately public AI answers questions about Singapore banks — where it drifts on borrowing costs and complaint timelines.

Lawnise Research & Editorial team

Institutional byline · published by Lawnise

Ask a public AI assistant what your bank charges for a card balance or a cash advance, or how fast it has to acknowledge a complaint, and you'll get an answer that sounds settled — specific, confident, often delivered with a tidy figure. The fact it's describing is a public one: the bank's own tariff sheet, its complaints policy, its product page. We checked the answers against those published facts, one by one.

Public AI doesn't get Singapore banking uniformly wrong — many answers align with the published record. But a recurring few don't, and where they go wrong, they go wrong by a wide margin, in the places a customer acts on them: the cost of borrowing and the handling of a complaint. These aren't rounding errors. This is one of several market-and-sector readings in our barometer, and the misstatements here echo the shape we see across the others.

How we checked AI answers about Singapore banks

In June 2026 we put high-intent retail questions — the kind a customer types before opening a product, disputing a charge, or working out what borrowing will cost — to a set of public AI systems, among them ChatGPT, Gemini, Copilot, Perplexity, Grok and Google AI Overview. Each answer about a Singapore bank was compared against that bank's own published facts: the disclosure sheet, the complaints policy, the product page. Where an answer conflicted with the published record, we flagged it for review, and we hand-verified each finding below against the live source before standing behind it.

This is a preliminary reading, and we'd rather say so plainly than dress it up. It covers a single month, so it's a baseline rather than a trend. And we report patterns, not a scoreboard — we name the AI systems only as the set we tested, never to rank one against another, because the more useful question is what they get wrong in common. The banks themselves we don't name either: institution names and source URLs are withheld to preserve the anonymised research design, and we retain the underlying evidence and result identifiers internally for audit and right-to-reply.

Where AI answers about Singapore banks drift

A few things recurred often enough in Singapore banking to be worth a risk owner's attention. None is a flat reversal of the bank's position. Each is the quieter failure — a published number stretched well past what it actually says, in a place where a customer reads it, plans around it, and only later finds the record was different.

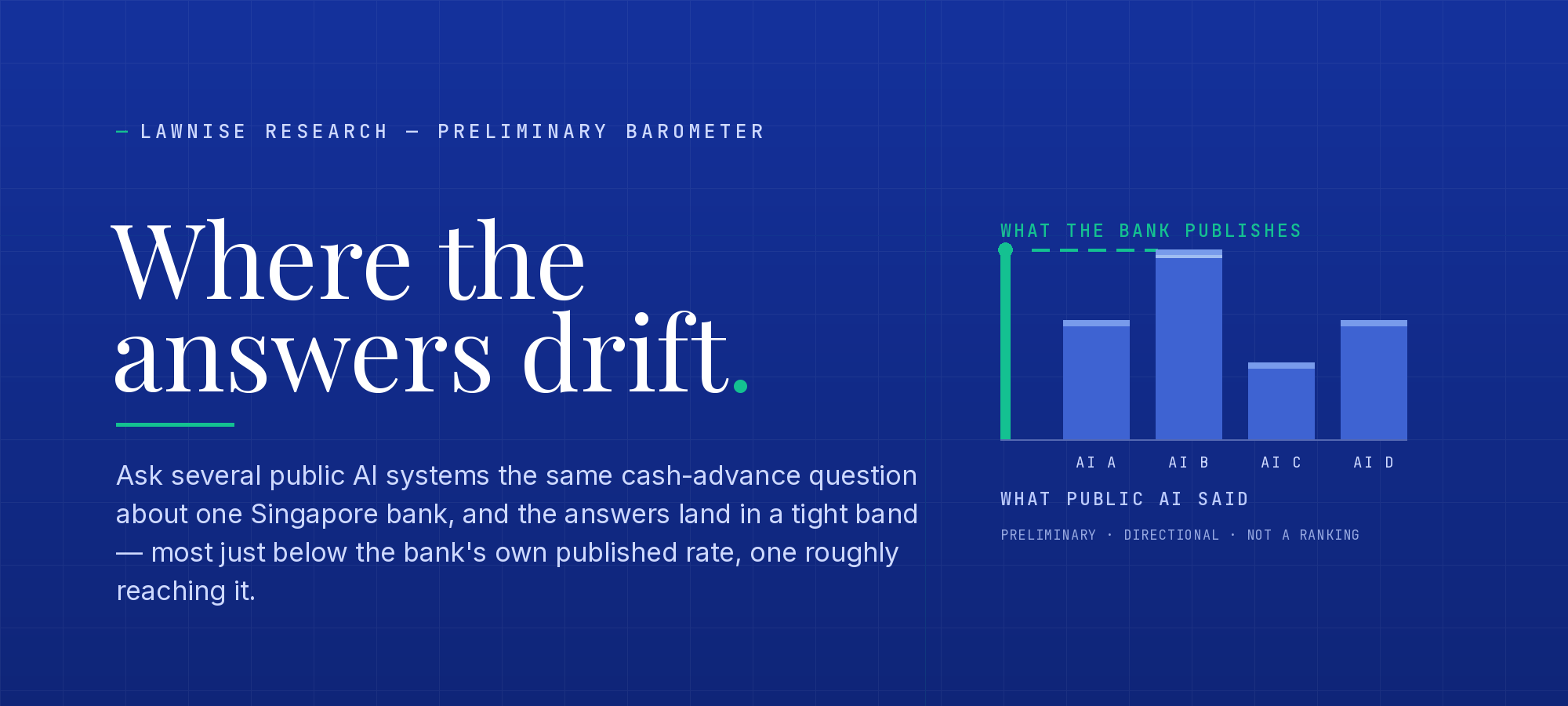

Every system that quoted a specific cash-advance rate put it below the published figure — and the one that wasn't wrong only avoided it by hedging into a range. The clearest miss sat on borrowing cost, and it wasn't a single stray answer. One major Singapore bank publishes a cash-advance interest rate of 28.5% per annum. We asked four systems. The three that committed to a specific number all came back below that figure — 26.9% at the lowest, with two systems both landing at 27.8%. The fourth didn't get it wrong, but it didn't get it right either: instead of a number it gave a range — 28% to 28.5% — that happened to span the published rate. So the honest reading isn't "everyone missed." It's sharper than that: every system that committed to a figure understated it, and the only system that wasn't wrong sidestepped the question with a range rather than a rate. A customer comparing the cost of a short-term withdrawal is either being told, with confidence, that it's cheaper than the bank's own published rate — or being handed a band so wide it settles nothing.

The most dramatic single miss was on a card balance, quoted at roughly half its real level. The largest gap in magnitude turned up on credit-card pricing, at a different major Singapore bank — and it was a single answer, not a pattern. That bank publishes a card purchase interest rate of 27.9% per annum. Asked about that prevailing rate, an assistant quoted 15–18% a year — a little over half of what the bank actually charges. To its credit, that assistant said outright that it lacked live access to current rates and pointed the customer to the disclosure sheet. The hedge is honest, and worth crediting. It's also easy to scroll past, and the number that sticks is the wrong one — a borrowing cost a customer would plan around as if it were roughly half of what they'll really pay.

The complaints clock ran more than twice as slow. Service timelines were the other soft spot, back at the first bank — the same one with the cash-advance gap. It commits, in writing, to acknowledge a customer complaint within 2 business days. Asked how quickly the bank acknowledges a complaint, an assistant said within 5 business days — more than double the committed window. A customer told the longer window plans around the longer window, and then feels misled when the bank's actual, shorter commitment turns out to be the real one. This isn't the dramatic kind of error, but it's the kind that erodes trust at exactly the moment a customer is already unhappy.

There's a fourth pattern we want to flag rather than feature. On questions about complaint resolution windows at a different bank, the AI answers conflicted with the bank's stated response time — but the bank's own published record draws a line between acknowledging, responding to, and resolving a complaint that the answers blurred. The contradiction may be real; it may also be an artefact of three different clocks being compared as one. We're holding this for a closer look before we lean on it, which is the point of saying it out loud.

Why AI answer accuracy is a governance risk for banks

None of these answers were written by the bank, and none of them can be edited by the bank. That's precisely the difficulty. A Singapore institution can keep its disclosure sheet immaculate and its complaints policy current — at one bank the cash-advance rate really is 28.5% and the acknowledgement commitment really is two business days; at another the published card rate really is 27.9% — and a customer can still walk in having been told a borrowing cost below the real one, or roughly half the real one, or a complaint deadline more than twice as long, by a system the bank has no contract with and no visibility into. The records were right. The representation circulating about them wasn't. And the consequences — confusion, an avoidable complaint, a fair-dealing question about information circulating in the bank's name — are the bank's to understand, evidence, and manage, regardless of who typed the answer.

Most governance frameworks weren't built to see this. They scrutinise what the institution publishes. This risk lives one step outside that perimeter, in the growing share of customers who ask an AI before they ask the bank.

The Singapore context makes the issue sharper: card usage is common, scams are an active policy concern, and bank disclosure standards are closely scrutinised. The errors we saw aren't random noise — they cluster on cost and on the handling of complaints, two areas where a misled customer has a concrete grievance and the bank has a concrete obligation. A 28.5% cash-advance rate put below the published figure by every system that quoted a specific number — 26.9% at the lowest — is the kind of thing a customer compares on, before the decision is made. A 27.9% card rate quoted as 15–18% is the kind of thing a customer discovers on a statement, after the decision is made. A two-business-day commitment quoted as five sets an expectation the bank then beats — or appears to break — through no fault of its own service. Neither is exotic; both are the everyday texture of retail banking, which is exactly why getting ordinary retail-banking facts this wrong, invisibly, is worth a risk function's time.

How to govern AI answers about your bank

The answer isn't to chase the AI, which can't be corrected the way the bank's own website copy can, but to govern the surface with the same seriousness applied to any channel that speaks in the bank's name. In practice that's a repeatable loop: watch what the major systems are telling customers; check it against the bank's own published facts; separate the genuine misstatements from the false alarms before acting on either; work out why a real one drifted, since a stale source and outside misinformation call for different fixes; rank what could actually mislead a customer — a card rate quoted at roughly half, say — ahead of what's merely imprecise; and keep a dated record of what was said and when. Done steadily, an open-ended worry becomes a managed process — the institution finds out before the customer does, corrects the sources it controls, and can show its work to a board, or to a regulator, when asked what it's doing about AI.

Read on

This is an early read from an ongoing barometer Lawnise is building on how public AI answers questions about Singapore banking, with more categories to follow over time. If you'd like to see what public AI is currently saying about your own institution — checked, the way these were, against your own published facts — we can scope a private baseline: sector-context, no obligation.

How to cite this

- Short form

- Lawnise Research & Editorial team. (2026). The State of AI Answer Accuracy in Singapore Banking — A Preliminary Barometer. Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-singapore-banks

- Long form (APA)

- Lawnise Research & Editorial team. (2026, June 23). The State of AI Answer Accuracy in Singapore Banking — A Preliminary Barometer (Methodology v1.1). Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-singapore-banks

- BibTeX

@misc{lawnise2026aiansweraccuracysingaporebanks, author = {Lawnise Research and Editorial team}, title = {The State of AI Answer Accuracy in Singapore Banking — A Preliminary Barometer}, year = {2026}, publisher = {Lawnise}, url = {https://www.lawnise.com/research/ai-answer-accuracy-singapore-banks} }

References

- [1]Lawnise Methodology (v1.1). Findings in this barometer are drawn from a single-month capture in which high-intent retail-banking questions were put to a set of public AI systems, and each answer about a Singapore bank was checked against that bank's own published facts. Each featured finding was true-positive verified — quote-grounded in the AI's full response and confirmed against the live published source — before publication. Reported as directional patterns, not a ranking of AI systems. Institution names and exact source URLs are withheld from public surfaces to preserve the anonymised research design; the underlying evidence and result identifiers are retained internally for audit and right-to-reply. https://www.lawnise.com/trust-index/methodology/v1#main