Market + AI Trend Intelligence

The State of AI Answer Accuracy in Singapore's Insurance Sector — A Preliminary Barometer

A preliminary Lawnise study of how accurately public AI answers questions about Singapore's insurance schemes — where it drifts on eligibility, dispute limits and cover.

Lawnise Research & Editorial team

Institutional byline · published by Lawnise

Picture someone in Singapore caring for an ageing parent, wondering whether the parent is disabled enough to start drawing a lifelong CareShield Life payout. Before calling anyone, they ask a public AI assistant. The answer comes back fast and confident, framed as if the rule were simple and settled. The fact it's describing is a public one — set out on the scheme's own government page. The trouble is that confidence and correctness are not the same thing, and at a moment like this the gap between them is the whole question.

Public AI doesn't get Singapore insurance wrong across the board — on several of the same questions, other tested systems answered correctly. But a recurring few misstate the rules in the places a consumer acts on them: who qualifies for a payout, what a dispute scheme will actually hear, what is and isn't protected. These aren't rounding errors. This is one of several sector readings in our barometer, and the misstatements here echo the shape we see across the others.

How we checked AI answers about Singapore insurance

In June 2026 we put high-intent questions — the kind a person types before relying on a payout, taking a dispute somewhere, or working out what's protected — to a set of public AI systems, among them ChatGPT, Gemini, Copilot, Perplexity, Grok and Google AI Overview. Each answer about a Singapore insurance scheme was compared against that scheme's own official page: CareShield Life, FIDReC, FIDReC-NIMA, the Policy Owners' Protection Scheme. Where an answer conflicted with the published record, we flagged it for review, and we hand-verified each finding against the official source before standing behind it.

This first reading focuses on Singapore's public insurance and protection schemes — eligibility, dispute resolution, and what's protected — with more of the sector to follow as the barometer builds month on month. It is a preliminary reading, and we'd rather say so plainly than dress it up. It covers a single month, so it's a baseline rather than a trend. And we report patterns, not a scoreboard — we name the AI systems only as the set we tested, never to rank one against another, because the more useful question is what they get wrong in common. The schemes themselves are public authorities and programmes, so we name them and cite their official pages directly. The finding-level evidence and result identifiers behind each example are retained internally for audit and right-to-reply.

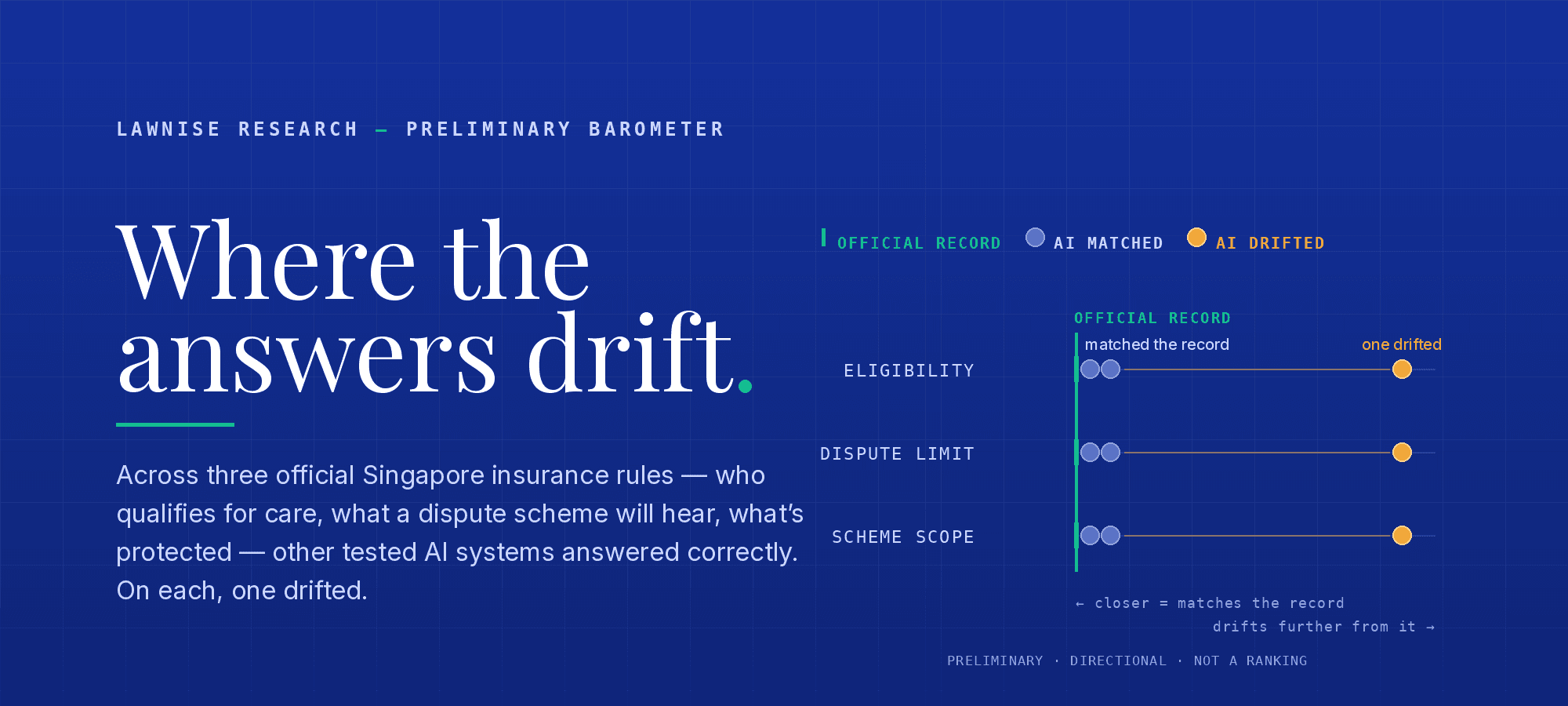

Where AI answers about Singapore insurance drift

A few things recurred often enough to be worth a risk owner's attention. Each is the quieter kind of failure — an official threshold, figure or scope stated as something it isn't, in a place where a consumer reads it, plans around it, and only later finds the record was different. Across the reviewed examples these were specific, system-level misses — not a uniform failure of every system tested.

On who qualifies for a CareShield Life payout, one system set the bar far below the real one — false reassurance at a high-stakes moment. The clearest miss sat on eligibility for a lifelong disability payout. Asked how disabled a person must be to start receiving CareShield Life payouts, one tested system answered that you qualify when unable to perform at least 1 of the 6 Activities of Daily Living (ADLs). The official trigger for severe disability, set out on the CareShield Life scheme's own page and assessed by an MOH-accredited assessor, is being unable to perform 3 of the 6 ADLs. This wasn't a fixed feature of how AI handles the question: other tested systems gave the 3-ADL threshold correctly. But where one got it wrong, the consequence is real. A person reading the lower bar could believe they qualify for a lifelong payout when they are well short of the threshold — building a care plan around money that, on the official rule, isn't yet due.

On the limit for a FIDReC-adjudicated dispute, one system quoted a ceiling more than three times the real one. The second miss sat on dispute resolution. Asked the current maximum claim limit for a dispute adjudicated by FIDReC, one tested system answered S$500,000 per case. The current limit, published on FIDReC's own site, is S$150,000 — raised from S$100,000 for claims filed on or after 1 July 2024. Here too another tested system answered with the correct figure, so this is one system's overstatement rather than a shared blind spot. The consequence falls on the consumer with a sizeable dispute: told the higher ceiling, they could take a large claim to FIDReC expecting it to be adjudicated, when a claim above S$150,000 falls outside what the scheme will hear — a wrong turn discovered only after committing to it.

On the FIDReC-NIMA motor scheme, one system described the scope broadly and partly backwards. The third miss was less a single wrong number than a wrongly drawn picture. Asked whether the FIDReC-NIMA scheme covers all motor disputes or only specific types, one tested system framed it as resolving disputes between drivers and their own insurers — when the scheme is for claims against the other party's insurer. It said only serious injuries or fatalities are excluded, when the scheme is non-injury entirely — all injury claims fall outside it — and it never mentioned the claim ceiling of S$3,000. On FIDReC's own page, the scope is narrow and specific: a non-injury motor accident claim against the other party's insurer, for an amount below S$3,000. A consumer with an injury claim, a claim against their own insurer, or a claim above S$3,000 could read this answer and wrongly believe NIMA applies to them — and steer toward a route that was never open.

There's a different pattern worth noting alongside these. On a separate question — the maximum protected under the Policy Owners' Protection Scheme for a life policy — a system answered the life-policy part adequately, then volunteered that general insurance such as motor, travel and property is "fully protected without limits." The PPF scheme, run by SDIC, is built around caps. Nobody asked about general insurance; the system added the reassurance unprompted, and the reassurance was wrong. It's the familiar shape of an assistant answering your question correctly, then offering a confident extra that you never asked for and can't easily tell is mistaken.

Why AI answer accuracy is a governance risk for insurers

None of these answers were written by the schemes, and none can be edited by them. That's precisely the difficulty. CareShield Life can keep its 3-ADL threshold plainly stated, FIDReC can keep its S$150,000 limit and its NIMA scope current — and a consumer can still arrive having been told that one ADL is enough, that half a million dollars is within reach, or that a motor scheme covers a claim it was never built for, by a system the scheme has no contract with and no visibility into. The records were right. The representation circulating about them wasn't. For insurers, scheme administrators, and the financial institutions whose customers sit downstream of these schemes, the consequences — a misdirected expectation, an avoidable complaint, a customer who feels misinformed about cover or eligibility — are theirs to understand, evidence, and manage, regardless of who typed the answer.

Most governance frameworks weren't built to see this. They scrutinise what the institution publishes. This risk lives one step outside that perimeter, in the growing share of consumers who ask an AI before they ask the insurer or the scheme.

The Singapore context makes the issue sharper: these schemes touch high-stakes, emotionally loaded decisions — long-term care, a contested claim, what survives an insurer failure — where a consumer is least able to sense that a confident answer is off. The errors we saw aren't random noise; they cluster on eligibility, on what a dispute scheme will hear, and on what's protected, three areas where a misinformed consumer has a concrete grievance. A 3-ADL threshold stated as one ADL is the kind of thing a family plans care around. A S$150,000 adjudication limit quoted as S$500,000 sends a large dispute down a path it can't take. A non-injury, sub-S$3,000 scheme described as broadly available invites the wrong claims in. The same shape shows up in our reading of Singapore banking, which suggests this isn't a quirk of one sector but a pattern in how public AI handles precise, official facts.

How to govern AI answers about your institution

The answer isn't to chase the AI, which can't be corrected the way an institution's own website copy can, but to govern the surface with the same seriousness applied to any channel that speaks in the institution's name. In practice that's a repeatable loop: watch what the major systems are telling consumers about your products and the schemes they sit alongside; check it against the official published facts; separate the genuine misstatements from the false alarms before acting on either; work out why a real one drifted, since a stale source and outside misinformation call for different fixes; rank what could actually mislead a consumer — an eligibility threshold stated too low, say — ahead of what's merely imprecise; and keep a dated record of what was said and when. Done steadily, an open-ended worry becomes a managed process — the institution finds out before the customer does, corrects the sources it controls, and can show its work to a board, or to a regulator, when asked what it's doing about AI.

Read on

This is an early read from an ongoing barometer Lawnise is building on how public AI answers questions about Singapore's insurance sector, with more categories to follow over time. If you'd like to see what public AI is currently saying about your own institution and the schemes around it — checked, the way these were, against the official published facts — we can scope a private baseline: sector-context, no obligation.

How to cite this

- Short form

- Lawnise Research & Editorial team. (2026). The State of AI Answer Accuracy in Singapore's Insurance Sector — A Preliminary Barometer. Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-singapore-insurance

- Long form (APA)

- Lawnise Research & Editorial team. (2026, June 23). The State of AI Answer Accuracy in Singapore's Insurance Sector — A Preliminary Barometer (Methodology v1.1). Lawnise. https://www.lawnise.com/research/ai-answer-accuracy-singapore-insurance

- BibTeX

@misc{lawnise2026aiansweraccuracysingaporeinsurance, author = {Lawnise Research and Editorial team}, title = {The State of AI Answer Accuracy in Singapore's Insurance Sector — A Preliminary Barometer}, year = {2026}, publisher = {Lawnise}, url = {https://www.lawnise.com/research/ai-answer-accuracy-singapore-insurance} }

References

- [1]Lawnise Methodology (v1.1). Findings are drawn from a single-month capture in which high-intent questions about Singapore insurance schemes were put to a set of public AI systems, and each answer was checked against the scheme's own official page. Each featured finding was true-positive verified — quote-grounded in the AI's full response and confirmed against the live official source — before publication. Reported as directional patterns, not a ranking of AI systems. Finding-level evidence and result identifiers are retained internally for audit and right-to-reply. https://www.lawnise.com/trust-index/methodology/v1#main

- [2]Central Provident Fund Board (CPFB) / Ministry of Health (MOH), Singapore. CareShield Life payouts are triggered when an MOH-accredited assessor assesses the insured as unable to perform 3 of the 6 Activities of Daily Living (severe disability). https://www.cpf.gov.sg/member/healthcare-financing/careshield-life(accessed 2026-06-23)

- [3]Financial Industry Disputes Resolution Centre (FIDReC). FIDReC's maximum claim limit for adjudication is S$150,000 per claim for claims filed on or after 1 July 2024 (S$100,000 before that date). https://www.fidrec.com.sg/knowledgebase/article/KA-01013/en-us(accessed 2026-06-23)

- [4]Financial Industry Disputes Resolution Centre (FIDReC). The FIDReC-NIMA Scheme is limited to non-injury motor accident claims against the other party's (third-party) insurer, where the amount claimed is below S$3,000. https://www.fidrec.com.sg/knowledgebase/article/KA-01152/en-us(accessed 2026-06-23)

- [5]Singapore Deposit Insurance Corporation (SDIC). The Policy Owners' Protection (PPF) Scheme provides capped protection — it is built around limits (aggregate guaranteed-sum-assured and surrender-value caps per life assured per insurer; general-insurance protection is subject to scheme limits), not unlimited cover. https://www.sdic.org.sg/pp_entitlement/(accessed 2026-06-23)